You only appreciate the importance of systemic analysis once you see the kind of new knowledge it delivers. There is much talk of systemic analysis in finance but there is very little research on the subject, not to mention a regulatory vacuum.

We analyze stock markets on a daily basis. In particular, we focus on systemic aspects of global finance. A key feature of systems (or systems of systems) is resilience, the capacity to absorb shocks and destabilizing events (defaults of large banks/corporations, natural disasters, conflicts, etc.). The global financial system is exposed to shocks on a daily basis. See our recent blog on how we measured the response of global finance to Ukraine, Greece, or the VW scandal.

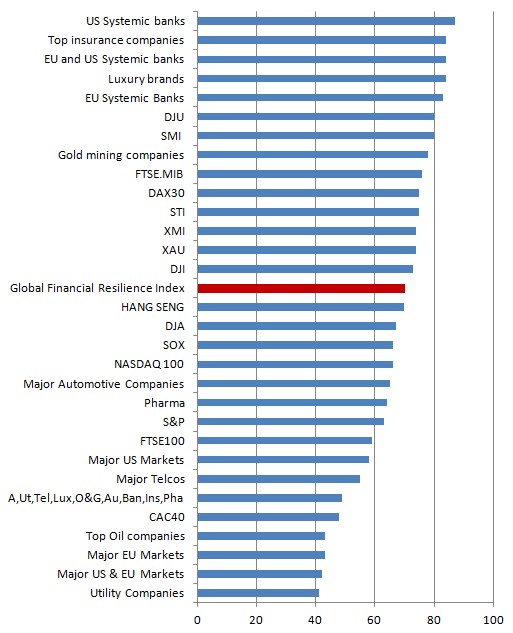

In this blog we illustrate how analyzing single markets or industry sectors can yield excessively optimistic results. The bar chart below lists the resilience of markets, systems of markets as well as sectors and systems thereof. Its importance to investors cannot be overstated.

A first example. Consider the following major EU markets (in parenthesis is the corresponding resilience in %):

A first example. Consider the following major EU markets (in parenthesis is the corresponding resilience in %):

FTSE.MIB (76), FTSE100 (59), CAC40 (48), DAX30 (75), SMI (80). Suppose now that we analyze them together, as a system. While the average resilience is 67.6%, the resilience of the system is a mere 43%, almost 25% less than the average. So much for linear thinking! The other point is that this system of markets does exist. We don’t run systemic analyses because it is fancy to do so, but because these systems actually do exist and therefore should be analyzed as such. Analyzing bits and pieces of a system in isolation is of little relevance. Systemic analysis should be the standard, not the exception.

A second case. Consider the following system of industries/sectors: Automotive (65), Utility (41), Telcos (55), Luxury (84), Oil & Gas (43), Gold Mining (78), Systemic Banks (84), Insurance (84) and Pharma (64). The resilience of these as a system is 49% while the mean is 66.4%. Again, a difference well over 15%.

A third case. Consider two huge systems of systems: US markets (58) and EU markets (43). When we put these together and analyze them as one super-system we obtain a resilience of 42%, well below the mean value of 55.5%. Again, analyzing markets in isolation generally produces falsely optimistic results. Incidentally, it is interesting to note how the system of US markets is a 15% healthier (more resilient) than the European one. The same may be said of the US and EU systemic banks, although the difference is quite small.

It won’t escape the reader which are the most resilient sectors: banks, insurance, luxury brands. Surprising? Not really.

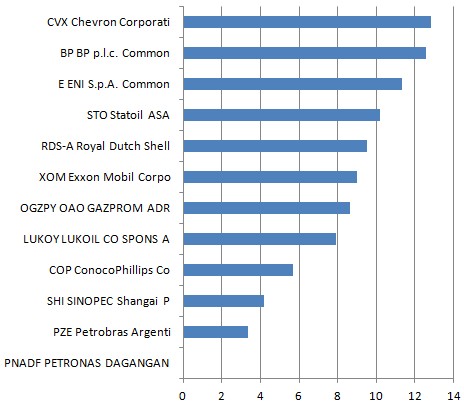

The information in the above chart, because of its exquisitely systemic flavour has a very low granularity. It can, of course, be made more granular. Take the Oil & Gas sector (a troubled industry, with a resilience of a mere 43%, which is not a good omen). The breakdown in terms of resilience contribution is as follows:

In other words, companies such as Chevron, BP and ENI, have a larger footprint on the Oil & Gas sector than, say, Sinopec or Conoco Phillips. In other words, Chevron, BP and EN are responsible for over 35% of the resilience of the Oil & Gas sector. Again, by footprint we mean resilience not market capitalization or revenue.

In other words, companies such as Chevron, BP and ENI, have a larger footprint on the Oil & Gas sector than, say, Sinopec or Conoco Phillips. In other words, Chevron, BP and EN are responsible for over 35% of the resilience of the Oil & Gas sector. Again, by footprint we mean resilience not market capitalization or revenue.

But why is all this resilience stuff so important to investors, especially to global and institutional investors? Resilience is intimately related to sustainability. In fact, resilience is what fuels sustainability. A fragile investment is not a sustainable investment. In a turbulent economic regime it is more important to be sustainable than to exhibit great performance for a quarter or two. Sustainability means survival. Especially in the face of future crises, market crashes and scandals.

The bottom line. If you’re looking into which sectors to invest and of which to stay out, run a systemic analysis. Start at the top and work your way down, not the other way around. Reality is far more non-linear than we can fathom. In a non-linear context A+B is not equal to B+A. This is not a linear world.

Numbers, not opinions. More soon.

By JM.

0 comments on “Sustainability and the Dramatic Importance of Systemic Analysis”