“Rating agencies? Do not speak evil of the dead” (Corriere della Sera, 15/1/2009). This is an extreme synthesis of the widespread opinion and of the doubts placed on rating agencies and on the value of the concept of rating. The sub prime crisis, Enron, Lehman Brothers, or Parmalat are just a few eloquent examples of how a business or a financial product may collapse shortly after being awarded a very high investment-grade rating. But are these isolated cases, which expose the weaknesses of rating processes, or just the tip of an iceberg? Our intention is to provide a critical overview of the concept of rating and to question its conceptual validity and relevance. We believe that the increasing levels of global uncertainty and inter-dependency – complexity in other words – as well as the socio-economic context of our times, will place under pressure and scrutiny not only the concept of rating, but all conventional end established risk management and Business Intelligence techniques. Unquestionably, the concepts of risk and risk rating lie at the very heart of our troubled global economy. The question is in what measure did rating contribute to the trouble and what, in alternative, can be done to improve or replace it altogether.The concept of rating is extremely attractive to investors and decision-makers in that it removes the burden of having to go over the books of a given company before the decision is made to invest in it or not. This job is delegated to specialized analysts whose work culminates in the rating. The rating, therefore, is an instrument of synthesis and it is precisely this characteristic that has made it so widespread. However, contrary to popular belief, a rating is not, by definition, a recommendation to buy or sell. Nor does it constitute any form of guarantee as to the credibility of a given company. A rating is, by definition, merely an estimate of the probability of insolvency or default over a certain period of time. In order to assign a rating, rating agencies utilize statistical information and statistical models which are used in sophisticated Monte Carlo Simulations. In other words, information on the past history of a company is taken into account (typically ratings are assigned to corporations which have at least five years of certified balance sheets) under the tacit assumption that this information is sufficient to hint what the future of the company will look like. In a “smooth” economy, characterized by prolonged periods of tranquility and stability this makes sense. However, in a turbulent, unstable and globalized economy, in which the “future is under construction” every single day, this is highly questionable.The process of rating, whether applied to a corporation or to a structured financial product, is a highly subjective one. The two main sources of this subjectivity are the analyst and the mathematical models employed to compute the probability of insolvency. It is in the mathematical component of the process that we identify the main weakness of the concept of a rating. A mathematical model always requires a series of assumptions or hypothesis in order to make its formulation possible. In practice this means that certain “portions of reality” have to be sacrificed. Certain phenomena are so complicated to model that one simply neglects them, hoping that their impact will negligible. As already mentioned, this approach may work well in situations dominated by long periods of continuity. In a highly unstable economy, in which sudden discontinuities are around every corner, such an approach is doomed for failure. In fact, the usage of models under similar circumstances constitutes an additional layer of uncertainty with the inevitable result of increasing the overall risk exposure. But there is more. In an attempt to capture the discontinuous and chaotic economy, models have become more complex and, therefore, even more questionable.In the recent past we have observed the proliferation of exotic and elaborate computer models. However, a complicated computer model requires a tremendous validation effort which, in many cases, simply cannot be performed. The reason is quite simple. Every corporation is unique. Every economic crisis is unique. No statistics can capture this fact. No matter how elaborate. Moreover, the complexity and depth of recently devised financial products has surpassed greatly the capacity of any model to embrace fully their intricate and highly stochastic dynamics, creating a fatal spill-over effect into the so-called real economy. We therefore stress with strength the fact that the usage of models constitutes a significant source of uncertainty which is superimposed on the turbulence of the global economy, only to be further amplified by the subjectivity of the analyst. In a discontinuous and “fast” economy no modeling technique can reliably provide credible estimates of the probability of insolvency, not even over short periods of time. It is precisely because of this fundamental fact that the concept and value of rating become highly questionable.

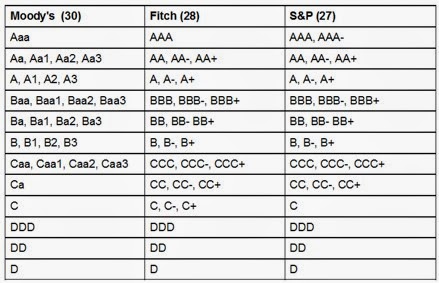

For most companies today, survival is going to be their measure of success. For example, an AA and BB rating indicate, respectively, a probability of insolvency of 1.45% and 24.57% within a period of 15 years. What is astonishing is not just the precision with which the probability is indicated, but the time span embraced by the rating. The degree of resolution – the number of rating classes – is unjustified in a turbulent economy. The fact that a rating agency can place a corporation in one of 25 or more classes indicates that there is sufficient “precision in the economy” and in the models to justify this fact. Clearly, the economy is not that precise. Table 1 indicates rating classes as defined by the three major rating agencies (number in parentheses indicates number of classes).

Table 1.

It is precisely this attempt to search for precision in a highly uncertain and unpredictable environment that casts many doubts on the concept, relevance and value of a rating. We basically sustain that the whole concept is flawed. We see the flaw in the fact that the process of assigning a rating is essentially attempting to do something “wrong” (compute the probability of insolvency) but in a very precise manner.An interesting parallel may be drawn between rating and car crash. Just like corporations, cars are also rated: for crashworthiness. Just like in the case of rating agencies, there exist different organisms that are certified to issue car crash ratings. A car crash rating is expressed by the number of stars – 1 to 5 – 5 being the highest. A car with a 5 star rating is claimed to be safe. Where is the problem? A crash rating is obtained in a test lab, in clinical conditions. What happens on the road is a different story. A crash rating tells you what happens under very precise but unrealistic conditions. In reality, a car will collide with another car traveling at an unknown speed, of unknown mass, with an unknown angle, and not with a fixed flat cement wall at 55 kph and at 90 degrees. So, a crash rating attempts to convey something about the future it cannot possibly catch. Just like in the case of corporate rating, computer crash simulations use state of the art stochastic models, are computationally very intensive and attempt to provide precise answers for unknown future scenarios.In summary, rating is an instrument which, directly or indirectly, synthesizes and quantifies the uncertainty surrounding a certain corporation or a financial product, as they interact with the respective ecosystems. This not only is extremely difficult but, most importantly it misses the fundamental characteristic of our economy and namely it’s rapidly increasing complexity. This complexity, which today may actually be measured, contributes to a faster and more turbulent ecosystem with which companies will confront themselves in their struggle to remain in the marketplace. This new scenario suggests new concepts that go beyond the concept of rating. Corporate complexity, as will be shown, occupies a central position.

Complexity, when referred to a corporation, can become a competitive advantage providing it is managed. However, we identify excessive complexity as the main source of risk for a business process. In particular, high complexity implies high fragility, hence vulnerability. In other words, excessively complex corporations are exposed to the Strategic Risk of not surviving in their respective marketplaces. Evidently, high fragility increases the probability of default of insolvency. The concept is expressed synthetically via the following equation:

C_corporation X U_ecosystem = Fragility

The significance of this simple equation is very clear: the fragility of a corporation is proportional to its complexity and to the uncertainty of the marketplace in which it operates. Complexity amplifies the effects of uncertainty and vice-versa. In practice what the equation states is that a highly complex business can survive in an ecosystem of low uncertainty or, conversely, if the environment is turbulent, the business will have to be less complex in order to yield an acceptable amount of fragility (risk). High complexity implies the capacity to deliver surprises. In scientific terms, high complexity manifests itself in a multitude of possible modes of behavior the system can express and, most importantly, in the capacity of the system to spontaneously switch from one such mode to another and without early warning. The fragility in the above equation is proportional to the strategic risk of being “expelled” from the marketplace.

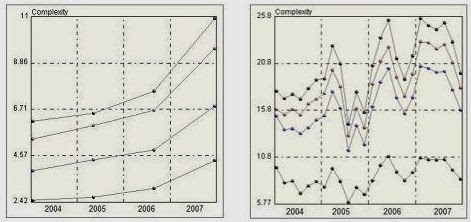

The weakness of the concept of rating is rooted in the fact that it focuses exclusively on the uncertainty aspects of a corporation without taking complexity into account. Clearly, as equation 1 shows, uncertainty is only part of the picture. In more stable markets, neglecting complexity did not have major consequences. In a less turbulent economy, business fragility is indeed proportional to uncertainty. When turbulence becomes the salient characteristic of an economy, complexity must necessarily be included in the picture as it plays the role of an amplification factor. In fact, the mentioned turbulence is a direct consequence of high complexity (the capacity to surprise and switch modes).The constant growth of complexity of our global economy has recently been quantified, in an analysis of the GDP evolution of the World’s major economies. It is interesting to note how in the period 2004-2007 the global economy has doubled its complexity and how half of this increment took place in 2007 alone, see Figure 1. Similarly, one may observe how the complexity of the US economy also grew albeit in the presence of strong oscillations, denoting an inherently non-stationary environment.

Figure 1. Evolution of complexity (second curve from bottom) of the World and US economies on the period 2004-2007.

The evolution of complexity, and in particular its rapid changes, act as crisis precursors. Recent studies of the complexities of Lehman Brothers, Goldman Sachs and Washington Mutual, as well as of the US housing market, have shown how in all these cases a rapid increment of complexity took place at least a year before the information of their difficulties became of public domain.Today it is possible to rationally and objectively measure the complexity of a corporation, a market, and a financial product or of any business process. Complexity constitutes an intrinsic and holistic property of a generic dynamic system, just like, for example, energy. Evidently, high complexity implies high management effort. It also implies the capacity to deliver surprises. This is why humans prefer to stay away from highly complex situations – they are very difficult to comprehend and manage. This is why, with all things being equal, the best solution is the simplest that works. But there is more. Every system possesses the so-called critical complexity – a sort of physiological limit, which represents the maximum amount of complexity a given system may sustain. In proximity of its critical complexity, a business process becomes fragile and exposed hence unsustainable. It is evident, that the distance from critical complexity is a measure of the state of health or robustness. In 2005 Ontonix has developed rational and objective measures of complexity and critical complexity, publishing templates for a quick on-line evaluation of both of these fundamental properties of a business process. The templates are based on financial highlights and standard balance sheet entries.

The fundamental characteristic of the process of complexity quantification is that it doesn’t make use of any mathematical modeling technique (stochastic, regression, neural networks, statistics, etc.). The method in fact is a so-called model-free technique. This allows us to overcome the fundamental limitation of any model which, inevitably, involves simplifications and hypotheses which, in most cases, are rarely verified. As consequence, the method is objective. Data is analyzed as is, without making any assumptions as to their Gaussianity and continuity and without any pre-filtering of pre-conditioning. As a result, no further uncertainty, which would contaminate the result, is added. At this point it becomes evident how complexity can occupy a central position in a new approach to the problem of rating. It is in fact sufficient to collect the necessary financial data, compute the complexity and corresponding critical value and to determine the state of health of the underlying business as follows:

State of health of corporation = Critical complexity – current complexity

The closer to its critical complexity the more vulnerable is the business. Simple and intuitive. A paramount property of this approach is that, unlike in the case of a rating, it does not have a probabilistic connotation. In other words, no mention is made as to the future state of the corporation. All that is indicated is the current state of health, no prediction is advanced. The underlying concept is: a healthy organization can better cope with the uncertainties of its evolving ecosystem. The stratification of the state of health (or fragility) is operated on five levels: Very Low, Low, Medium, High and Very High. In highly turbulent environments, attempting to define more classes of risk is of little relevance. It is impossible to squeeze precision of out of inherently imprecise systems.

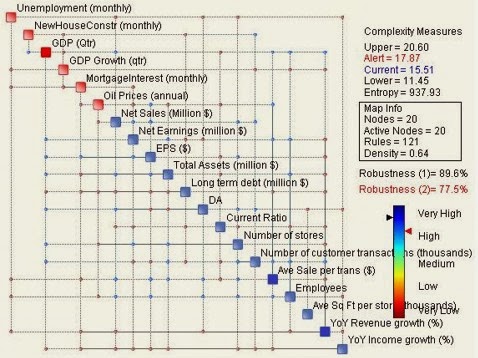

Let us illustrate the above concepts with an example of a publicly traded company. The computation of the state of health (rating) has been performed using fundamental financial parameters (see blue nodes in the graph in Figure 2) as well as certain macro-economic indicators (red nodes) which represent, albeit in a crude manner, the ecosystem of the corporation. Figure 2 illustrates the so-called Complexity & Risk Map of the corporation as determined using the on-line rating system developed by Ontonix (www.ontonix.com). The parameters of the business are arranged along the diagonal of the graph, while significant relationships between these parameters are represented by the connectors located away from the diagonal. Needless to say, the said relationships are determined by a specific model-free algorithm, not by analysts. The health rating of the company is “Very High” and corresponds, in numerical terms, to 89%. The map also indicates the so-called hub, or dominant variables, indicated as nodes of intense red and blue color.

Figure 2. Complexity & Risk Map of a corporation, indicating the corresponding health rating (business robustness).

The conventional concept of rating – intended as a synthetic reflection of the probability of insolvency – has shown its inherent limitations in a global, turbulent and fast economy. The proof lies in the crippled economy. The usage of mathematical models, as well as the subjectivity of the rating process, adds a further layer of uncertainty which is invisible to the eyes of investors and managers. Under rapidly changing conditions and in the presence of high complexity, the concept of probability of default is irrelevant. Instead, a more significant rating mechanism may be established based on the instantaneous state of health of a corporation, as its capacity to face and counter the uncertainties of its marketplace. In other words, the (strategic) risk of not being able to survive in one’s marketplace is proportional to the mentioned state of health. The capacity of a corporation to survive in its market place does not only depend on how turbulent the marketplace is but, most importantly, on how complex the corporation is. This statement assumes more importance in a highly turbulent economic climate. If corporations do not start to proactively control their own complexity, they will quickly contribute to increasing even more the turbulence of the global marketplace, making survival even more difficult. Complexity, therefore, is not just the basis of a new rating mechanism, it establishes new foundations of a superior and holistic form of Business Intelligence.

0 comments on “The Present and Future of the Concept and Value of Ratings”