Much has been written about the global economic crisis, its causes and its consequences. We could say that to a large extent we actually understand what has happened and why. The point, however, is to look to the future and to learn from past mistakes. In particular, we would all like to understand how to avoid the next crisis which, because of the increasing fragility of the global economy, with all likelihood will be more severe than the current one. Of all the causes which have contributed to the crisis we identify ratings, and rating agencies in particular, as the single key factor. In fact, according to the Financial Crisis Inquiry Committee in January 2011: “The three credit rating agencies were the key enablers of the financial meltdown”.

Much has been written about the global economic crisis, its causes and its consequences. We could say that to a large extent we actually understand what has happened and why. The point, however, is to look to the future and to learn from past mistakes. In particular, we would all like to understand how to avoid the next crisis which, because of the increasing fragility of the global economy, with all likelihood will be more severe than the current one. Of all the causes which have contributed to the crisis we identify ratings, and rating agencies in particular, as the single key factor. In fact, according to the Financial Crisis Inquiry Committee in January 2011: “The three credit rating agencies were the key enablers of the financial meltdown”.

Credit rating agencies play a pivotal role in the economy. They process, filter, and funnel information from the financial industry and economy in the form of ratings to investors. Markets and investors rely heavily on this information. However, ratings are:

- expensive

- subjective

- opaque, unregulated

- not suited for a turbulent economy

It is not difficult to imagine how conflict of interest fits into the picture. In fact rating agencies are controlled by huge investment funds. This makes them tremendously powerful and they continue to thrive in a business-as-usual fashion, as if nothing had happened. That is a reflection of immense power. In effect, a downgrade of a country’s economy by a single notch means billions of losses for that country. Overnight. Moreover, it is the rated entity that pays for the rating, not those who use it. In past, investors purchased reports containing ratings of specific companies, today, ratings are available for free. It is difficult how such a process can be free of conflicts of interest.

Until we can break the above scheme, there is no real reason to believe that situation will change. But, breaking the scheme, given the power concentrated in the hands of the rating agencies, is almost a practical impossibility. Therefore, a different approach is necessary. If credit rating agencies are left to operate then they will surely spark another crisis. This is because the global economy has been crippled and is very fragile. It cannot take a second severe blow.

The sub-prime crisis, Enron, Lehman Brothers, or Parmalat are just a few eloquent examples of how a business or a financial product may collapse shortly after being awarded a very high investment-grade rating. This article provides a critical overview of the concept of rating and questions its conceptual validity and relevance. We believe that the increasing levels of global uncertainty and interdependency – complexity in other words – as well as the socioeconomic context of our times calls for a different and better rating scheme.

The concept of rating is extremely attractive to investors and decision-makers in that it removes the burden of having to go over the books of a given company before the decision is made to invest in it or not. This job is delegated to specialized analysts whose work culminates in the rating. The rating, therefore, is an instrument of synthesis and it is precisely this characteristic that has made it so widespread. However, contrary to popular belief, a rating is not, by definition, a recommendation to buy or sell. Nor does it constitute any form of guarantee as to the credibility of a given company. A rating is, by definition, merely an estimate of the probability of insolvency or default over a certain period of time. In order to assign a rating, rating agencies utilize statistical information and sophisticated statistical models. In other words, information on the past history of a company is taken into account under the tacit assumption that this information is sufficient to hint what the future of the company will look like. In a “smooth” and “slow” economy, characterized by prolonged periods of tranquility and stability this maybe makes sense. However, in a turbulent, unstable and globalized economy, in which the “future is under construction” every single day, this is highly questionable.

The process of rating, whether applied to a corporation or to a financial product, is a highly subjective one. The two main sources of this subjectivity are the analyst and the mathematical models employed to compute the probability of insolvency/default. It is in the mathematical component of the process that we identify the main weakness of the concept of a rating. A mathematical model always requires a series of assumptions or hypotheses in order to make its formulation possible. In practice this means that certain “portions of reality” have to be sacrificed. Certain phenomena are so complicated to model that one simply neglects them, hoping that their impact will negligible. In a highly unstable economy, in which sudden discontinuities are around every corner, such an approach simply doesn’t work. In fact, the usage of models under similar circumstances constitutes an additional layer of uncertainty with the inevitable result of increasing the overall risk exposure. But there is more. In an attempt to capture the discontinuous and chaotic economy, models have become more complex and, therefore, even more questionable. It is a vicious circle.

The other characteristic of ratings which looks suspicious is their “precision”. For example, AA and BB ratings indicate, respectively, a probability of insolvency of 1.45% and 24.57% within a period of 15 years. What is astonishing is not just the precision with which the probability is indicated, but the time span embraced by the rating. The degree of resolution – the number of rating classes – is unjustified in a turbulent and complex economy. The fact that a rating agency can place a corporation in one of 25 or more classes indicates that there is sufficient “precision in the economy” and in the mathematical models to justify this fact. The table below indicates rating classes as defined by the three major rating agencies (number in parentheses indicates number of classes).

| Moody’s (30) | Fitch (28) | S&P (27) |

| Aaa | AAA | AAA, AAA- |

| Aa, Aa1, Aa2, Aa3 | AA, AA-, AA+ | AA, AA-, AA+ |

| A, A1, A2, A3 | A, A-, A+ | A, A-, A+ |

| Baa, Baa1, Baa2, Baa3 | BBB, BBB-, BBB+ | BBB, BBB-, BBB+ |

| Ba, Ba1, Ba2, Ba3 | BB, BB- BB+ | BB, BB- BB+ |

| B, B1, B2, B3 | B, B-, B+ | B, B-, B+ |

| Caa, Caa1, Caa2, Caa3 | CCC, CCC-, CCC+ | CCC, CCC-, CCC+ |

| Ca | CC, CC-, CC+ | CC, CC-, CC+ |

| C | C, C-, C+ | C |

| DDD | DDD | DDD |

| DD | DD | DD |

| D | D | D |

However, Nature doesn’t admit that much precision and neither does the economy. Why are hotels rated on a scale from 1 to 5 stars and not from 1 to, say 25 stars? Why is the crashworthiness of automobiles rated on a scale from 1 to 5 stars? Why are there only 4 classes of cardiac infarction risk and not 20? It is because the degree of precision in Nature is dictated by physics and, ultimately, by logic and reason. In a real world, there is no difference between a probability of failure of 1% or 1.1% Evidently the rating agencies have conceived so many risk classes because they need them to justify a very profitable business.

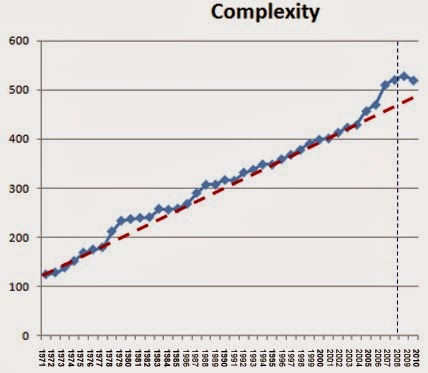

As the economy becomes more turbulent and complex, such a high number of risk classes will be less justified. In fact, as things get more complex, they automatically become less precise – this is known as the Principle of Incompatibility (high complexity is incompatible with high precision). Using data from the World Bank we have computed the evolution of complexity of the World as a system. The result is illustrated in Figure 1.

Figure 1. Evolution of global complexity in the period 1971-2010.

Complexity reveals, in this case, how interconnected and interdependent the World is. In practice it “measures the degree of globalization” as well as its pace. It is interesting to note how after 2008 this pace has slowed down. However, over the last 40 years, complexity has been growing at almost a constant rate.

In a similar fashion we have computed the evolution of global turbulence. The plot is illustrated in Figure 2. Turbulence measure how chaotic the world is becoming and it too has been growing steadily over the years.

Figure 2. Evolution of global turbulence in the period 1971-2010.

The tendency is almost the same except the fact that there has been an acceleration of “turbulence production” after the Berlin Wall came down (see vertical line in correspondence of 1989). Now, in an economy characterized by high (and growing) complexity and high turbulence a rating cannot be stratified into over 25 classes. It simply doesn’t make sense.

The conventional concept of rating – intended as a reflection of the probability of insolvency – has shown its inherent limitations. The proof lies in the crippled economy. The usage of mathematical models, as well as the subjectivity of the rating process, adds a further layer of uncertainty which is invisible to the eyes of investors and managers. Under rapidly changing conditions and in the presence of high complexity, the concept of probability of default is disputable to say the least. Instead, a more significant rating mechanism may be established based on the resilience of a corporation, i.e. its capacity to face and counter the uncertainties and shocks of the economy. The capacity of a corporation to survive in its marketplace does not only depend on how turbulent the marketplace is but, most importantly, on how resilient the corporation itself is. Therefore, a modern rating system should focus on the resilience of business, not on the Probability of Default. Moreover, it should allow investors to quickly verify it. Today, it is a practical impossibility to check if a rating is really what a rating agency claims it to be.

Rating agencies have defended themselves saying that ratings express an opinion. However, given what is at stake, ratings should be a science and not an opinion. The global economy cannot afford to rely on subjective opinions and conflicts of interest. Ratings have been conceived in a turbulence-free world, and world that no longer exists. The logic and mathematics behind conventional ratings are not applicable in today’s economy. Either rating agencies will take this into account or they will progressively lose credibility – a process which has already started – and go out of business.

www.ontonix.com www.rate-a-business.com

0 comments on “Why Regulating Ratings Won’t Fix the Problem”