Warren Buffet said in 2003 that the derivatives market was “devised by madmen” and a “weapon of mass destruction”. Global GDP stands at $69.4 trillion while the derivatives market is today over $700 trillion. What this means is that the financial industry has run up phantom paper debts worth more than ten times what the entire planet produces in a year. Are Brownian motions, Wiener processes, martingales and Ito integrals worth that much? Not only this debt cannot be paid back, the heart of the matter lies in the extreme complexity of the construct which, to a large degree, is run by computers and which exhibits dynamics which nobody today is able to grasp and understand. It all looks more or less like this:

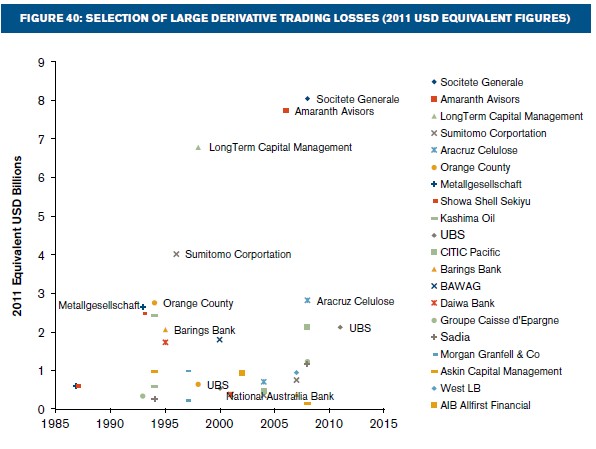

Derivatives are said to be very complex. Just how complex is that? Until one actually measures how complex a given derivative is, it is difficult to make any credible claims as to its amount of complexity. Sounds kind of obvious. But let’s suppose that this is indeed true. In effect, derivatives of derivatives (of derivatives…) seem to have been constructed in a fiendish way so as to confuse the non-expert investor. Very high complexity allows one to hide fraud, to cover up problems, incompetency, lax management, misunderstanding of the dynamics of the business etc., etc. This last aspect seems to have confused the experts too. Complex operations with complex products are likely to lead to unexpected outcomes and consequences. The figure below illustrates a selection of the largest recent derivative trading losses (Source: Operational Risk Modelling Framework, Milliman, February 2013).

Derivatives are said to be very complex. Just how complex is that? Until one actually measures how complex a given derivative is, it is difficult to make any credible claims as to its amount of complexity. Sounds kind of obvious. But let’s suppose that this is indeed true. In effect, derivatives of derivatives (of derivatives…) seem to have been constructed in a fiendish way so as to confuse the non-expert investor. Very high complexity allows one to hide fraud, to cover up problems, incompetency, lax management, misunderstanding of the dynamics of the business etc., etc. This last aspect seems to have confused the experts too. Complex operations with complex products are likely to lead to unexpected outcomes and consequences. The figure below illustrates a selection of the largest recent derivative trading losses (Source: Operational Risk Modelling Framework, Milliman, February 2013).

Of the $700 trillion of derivatives that are in the cyberspace $220 trillion is held by JPMorgan Chase, Citibank, Bank of America and Goldman Sachs, see below (source: US Department of Treasury):

Of the $700 trillion of derivatives that are in the cyberspace $220 trillion is held by JPMorgan Chase, Citibank, Bank of America and Goldman Sachs, see below (source: US Department of Treasury):

The interesting thing to note is that these banks are all very fragile. We’re not talking of performance in terms of stock price, the EPS or the bonuses of the management. Fragile is the opposite to resilient and what that equates to is total lack to absorb shocks, contagion or extreme events. In particular, all four of these systemic giants have an alarmingly low two-star Resilience Rating:

The interesting thing to note is that these banks are all very fragile. We’re not talking of performance in terms of stock price, the EPS or the bonuses of the management. Fragile is the opposite to resilient and what that equates to is total lack to absorb shocks, contagion or extreme events. In particular, all four of these systemic giants have an alarmingly low two-star Resilience Rating:

The analysis has been performed using publicly available Balance Sheet data and the Rating Alert System which has been launched recently by Ontonix and QBT. These banks are not Too Big To Fail, they are Too Complex To Survive. Today there is a very large number of potentially destabilizing events, ranging from conflicts to extreme climatic events (we’ve seen quite a few of these lately, haven’t we?) which could easily bring down any one of these banks. The remaining three would probably follow in a matter of hours, triggering a devastating shock wave which would engulf the entire economy – not just the financial industry – in a day or two. What can be done? First of all, we could start by dismantling the derivatives time-bomb (see recent blog). Second, corporations worldwide should robustify their respective businesses, in order to be better equipped for the inevitable upcoming financial tsunami.

We shall be monitoring closely the resilience of these four hubs of the global financial system. Stay tuned.

0 comments on “The Derivatives Time-Bomb”