The Probability of Default (PoD) of a company is the central concept behind a conventional rating. Ratings constitute a fundamental link between the markets and investors. Their importance cannot be overstated. However, traditional ratings, according to the Credit Rating Agencies themselves, are merely opinions. The process of computation of a Probability of Default of a company is not only subjective, it lacks transparency and, given the fact that it is not a strictly scientific process, it may be manipulated, leading to issues such as conflicts of interest and fraud.

The Big Three rating agencies have been providing ratings since the beginning of the 20-th century. The world was very different then. Traditional ratings have become dangerously outdated and, most importantly, not suited for a turbulent economy. As the complexity of the economy grows, conventional ratings produce results of increasing irrelevance. Mathematically correct but irrelevant. This has become apparent in 2007 when Credit Rating Agencies have misled investors and contributed significantly to the economy meltdown. The new rating concept introduced by Universal Ratings has been engineered specifically for turbulence and a fast economy dominated by shocks, bubbles and instability. Markets are not efficient. In Nature there is no such thing as equilibrium.

Conventional ratings will surely continue to be used in the foreseeable future. However, in order to provide investors with new knowledge and insights we propose a novel, objective complexity and resilience-based rating. Increasing complexity is, with all likelihood, the most evident and dramatic characteristic of the economy. It is also the hallmark of our times. Resilience is the capacity to withstand shocks and is a measurable physical quantity. A resilience-based rating is applicable to companies, stocks, portfolios, and funds, systems of companies or national economies. In our turbulent economy, which is fast, uncertain and highly interdependent, extreme and sudden events are becoming quite common. Such events will become more frequent and intense, exposing fragile businesses to apparently unrelated events originating thousands of kilometers away. This mandates that companies and investors focus not just on performance but also on resilience, building less complex, less fragile businesses. Resilience means survival and sustainability. But most importantly, our resilience-based ratings are science, not opinions.

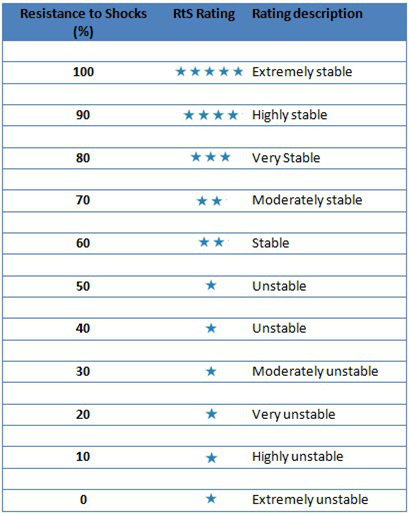

Resilience, or Resistance to Shocks (RtS) is measured on a scale from 0% to 100%. Values close to 100% denote high stability and ability to absorb turbulence and shocks. Low values, on the other hand, reflect vulnerability which may affect long-term sustainability.

The present blog provides Resistance to Shocks measures versus conventional ratings for approximately 500 companies listed on the S&P, the Dow and the NASDAQ. The analyses have been based on quarterly Standardized Balance Sheets.

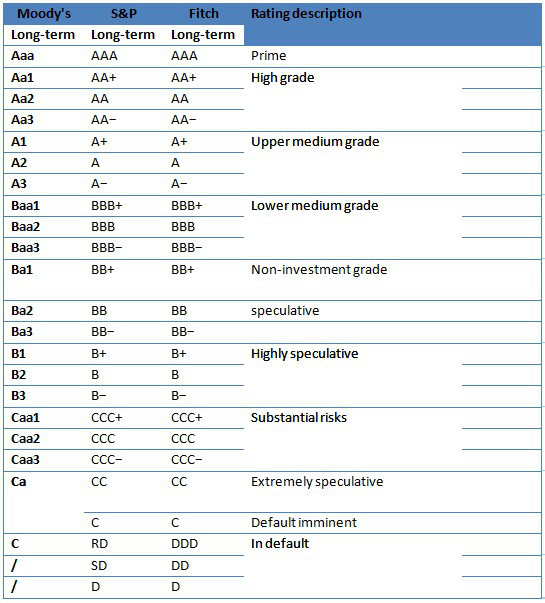

Credit Rating Agencies stratify risk (the Probability of Default) into numerous classes as shown in the table below.

UR’s Resistance to Shocks ratings do not measure the creditworthiness of a borrower nor its probability of default. Instead, RtS ratings provide an innovative measure of the stability of a corporation (or an investment portfolio) in the face of shocks and turbulence. Therefore, the two cannot be compared and no correspondence should be attempted as these ratings provide totally independent information.

The table below illustrates the stratification of Resistance to Shocks ratings:

An RtS rating is not yet another credit rating. However, it may be used to augment a conventional rating. In analogy to medicine, an RtS rating is not like a second opinion, it is more. It is a totally new piece of information. In effect, one may pair these ratings so as provide an integrated PoD-RtS rating and to answer the question: how good is a rating? How strong is it? Consider the following limit cases:

- Prime investment grade & High Resistance to Shocks – ‘Strong AAA’

- Prime investment grade & Low Resistance to Shocks – ‘Weak AAA’

- Speculative grade & High Resistance to Shocks – ‘Strong CCC’

- Speculative grade & Low Resistance to Shocks – ‘Weak CCC’

What these examples indicate is that a triple-A rating can hide fragility or that a triple-C rating may point to a situation of stability. In both cases, similar information is quite valuable. In practice, an RtS rating offers an additional discrimination mechanism when it comes to selecting stocks, asset classes or investment strategies. But not only that. An RtS rating offers an additional degree of comfort, a sort of insurance policy on top of a conventional PoD rating.

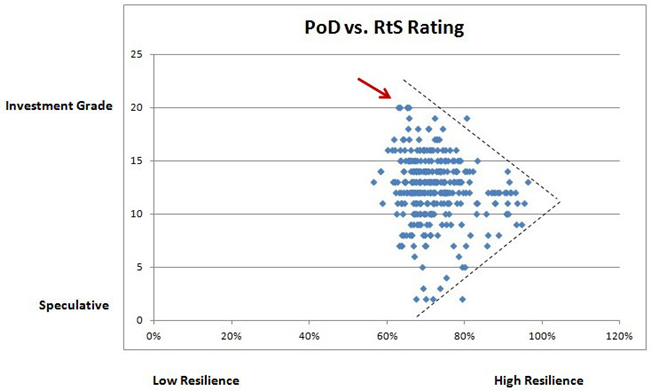

Almost 500 companies listed on the Dow, the S&P and the NASDAQ have been analysed based on their quarterly fundamentals. When we confront the two ratings, the situation is as indicated below (conventional ratings have been projected onto a scale from 0 to 20, where 0 corresponds to junk and 20 to Prime Investment Grade):

Of the nearly 500 companies, 5 are Prime Grade (see red arrow), another 3 one notch less and 5 two notches less. With only one exception, all of these have an RtS rating of 70% or less. The majority of the companies have a PoD rating in the Lower and Upper Medium Grade with a spread in terms of RtS rating in the 55% to 90% range. Finally 73 companies have a rating that is below Speculative Grade. With one exception, most have an RtS rating ranging from 60% to 75-80%.

In essence, we have a triangular domain which prompts the following conclusions (NB these apply only to the mentioned markets):

- Triple-A ratings do not correspond to companies with the highest Resistance to Shocks rating (their RtS rating is around 65%).

- Companies with the highest Resistance to Shocks rating have a Lower and Upper Medium Grade rating. Here the RtS rating spread is from 55% to 90%. Hence, Lower and Upper Grade ratings are the strongest (most reliable).

- Highly Speculative Grade ratings may, however, point to situations of relative stability (around 70%, even up to 80%). In other words, there is ‘stable junk’ out there.

The main conclusion of the study – which is currently being extending to all listed companies (approximately 45000) – is that triple-A ratings are generally weak.

Reblogged this on Calculus of Decay .

LikeLike